The European Commission’s (EC) requirements for sustainability reporting already affect a significant portion of investments made by companies. Certain areas, however – such as strategic liquidity management, cover-funds from direct employer pension commitments and lump-sum support funds for corporate pension plans – have been omitted from regulation so far. This could change if the legislator wants to achieve transparency without contradiction and ambiguity.

We think it likely the EC’s proposal for the Corporate Sustainability Reporting Directive could be expanded to include these areas. In order to avoid reputational risks that potentially weigh on enterprise values, executive management teams should therefore bring their company’s public image into harmony with their investment decisions among treasury and pension management departments. We outline the key aspects that should be taken into account.

European companies increasingly targeted by regulators

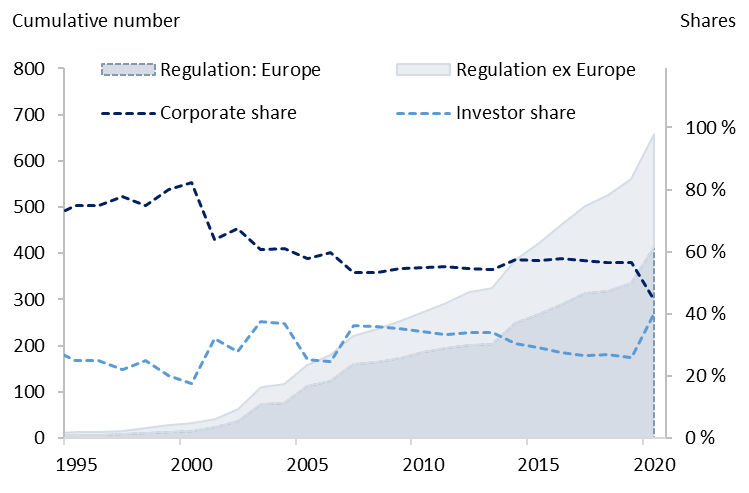

Regulation of sustainable investments is gaining momentum as national legislators aim to prevent empty promises, such as greenwashing. This should bring a higher level of transparency and reliability not only to financial product sales but also to corporate reporting. This legislative push is being driven forward mainly by the EC and EU member states, which have launched 63 percent of all the initiatives worldwide since the year 2000, according to the UN Principles for Responsible Investment (PRI). A recent surge was triggered in 2019 by the EU Green Deal, which specified the goals of the 2015 Paris Climate Agreement in more detail to help EU member states pave the way for a carbon-neutral economy by 2050.

Thus far, 60 percent of all sustainability-related regulations in the EU since the year 2000 affect companies; only a quarter of them affect investors. But recent suggestions for improvements to the directives Mifid II – which takes investors’ sustainability preferences into account – and Ucits – which considers sustainability-related risks in fund management – have caused this relatively stable ratio to change. Over the course of 2020-2021, the proportion of sustainability-related regulations that affect investors has risen to 40 percent.

Europe is in the lead when it comes to regulation of sustainable investments

Source: UN PRI, Metzler Asset Management

We expect this shift will increase the pressure, particularly on listed companies, to report consistently on sustainability aspects in their investments and to bring this into harmony with the public image they promote to stakeholders. Reporting inconsistencies and a lack of transparency can lead to reputational risks that have a negative impact on the value of the company and implicitly make refinancing via the capital markets more expensive. Critical NGOs and the media will focus more strongly on companies that say they are committed to upholding internationally recognized norms and standards but invest their own capital in securities that are burdened by severe controversies in these areas.

Capital investments should be in keeping with the company’s public image

What can companies do about it? Excluding securities from issuers that repeatedly attract negative attention due to controversial business practices or product exposure makes economic sense only to a certain extent. For example, when considering even minor controversies alongside moderate and severe cases, one would exclude 15 percent to 20 percent of the market capitalization in the European equity universe. Hence, the ex-ante tracking error of a portfolio would get disproportionately strained compared with the benchmark.

Companies should also focus on sound ESG integration, which incorporates financial-material aspects when analyzing investment alternatives according to ecological, social and good corporate governance guidelines in order to strengthen the risk-return profiles of the investment strategies. Two things are important in ESG integration: a systematic, closely interlinked and, above all, documented consideration of sustainability aspects in the investment process, and an effective risk management that identifies and counteracts misalignments without diluting sustainability criteria.

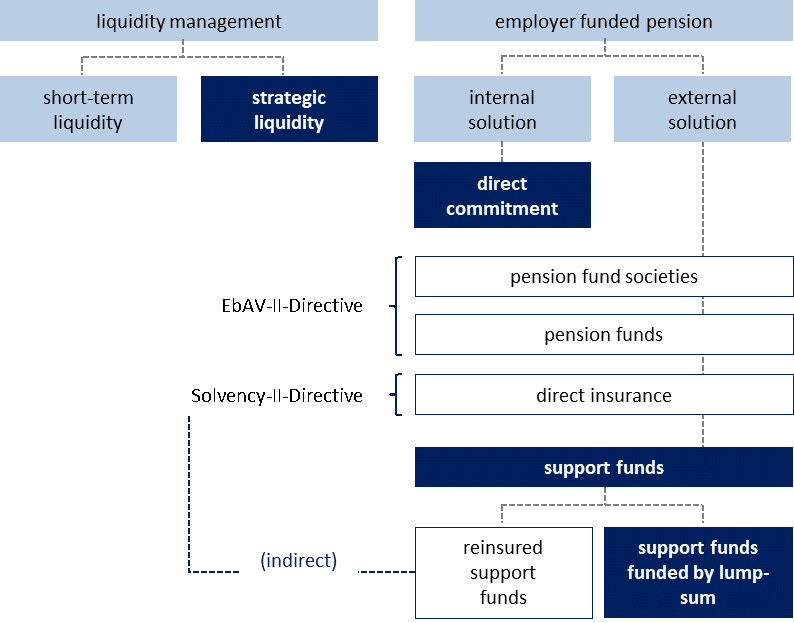

Consistent ESG integration according to these principles should apply to all areas of a company’s capital investment strategy that could fall under disclosure regulations in the foreseeable future, even if they have been excluded from regulation so far. This applies in particular to strategic liquidity management as well as to cover-funds from direct employer pension commitments and lump-sum support funds for corporate pension plans.

In Germany, for example, according to the Arbeitsgemeinschaft betriebliche Altersversorgung (a working group for corporate pensions), cover-funds from direct employer pension commitments and lump-sum support funds accounted for more than 50 percent of all corporate pension assets in 2018 – equivalent to 10 percent of the German economy’s gross domestic product.

Parts of corporate investing have previously been excluded from sustainability-related regulation (highlighted in dark blue)

Source: Metzler Asset Management

- Strategic liquidity refers to funds that are not directly required for day-to-day business. They are invested primarily in multi-asset strategies that are managed based on fundamental analysis. Depending on the risk tolerance and return expectations of the investor, allocation to the asset classes is derived from this. Professional ESG integration is particularly effective when multi-asset strategies are applied for structuring the various asset classes. It is not enough to focus on drivers of returns only. Risk management must also be adapted to sustainability criteria. This is the only way to offset any unintentional bias toward certain risk premiums, sectors or regions generated by sustainability preferences without diluting the investor’s individual sustainability goals.

- A direct commitment is one of five ways to implement a corporate pension scheme where companies voluntarily undertake to pay the employee a fixed amount directly from the company’s assets in the event of a pension claim. Direct commitments can be offset against pension provisions in the balance sheet with the help of contractual trust arrangements. Three things can be achieved by such a balance sheet contraction:

> Strengthening of earnings indicators such as the return on equity

> Improvement of financing conditions via a lower debt-equity ratio

> Reduction of administrative expenses and related costs.

But if the company does not disclose sustainability aspects among off-balance-sheet funds in the notes section of the annual accounts, investors will not be able to monitor the consistency of the company’s public image. The higher the share of funds that are taken off corporate balance sheets, the more likely it is that the regulator will take notice and look into this issue.

- This also applies to support funds funded by lump-sums, which account for about 6 percent of all support funds. Unlike reinsured support funds, it is not the product provider but the company that makes capital investment decisions. Permissible investment options include corporate and sovereign securities, precious metals, funds or even real estate in some cases. Thus, cover-funds also harbor potential reputational risks about which stakeholders – such as employees or investors – must be informed. The remaining parts of a company’s pension plan are covered by current regulation in terms of sustainability aspects: the EbAV-II directive covers pension funds and pension fund societies, and the Solvency II Directive covers direct insurance and indirect insurance for reinsured support funds.

Transparent companies can put their competitors under pressure

We do not expect initiatives for greater transparency to come from international organizations such as NGOs. According to the UN PRI, these and similar organizations have been responsible for only 2 percent of all sustainability-related investment regulations worldwide since the year 2000. By contrast, there are numerous examples of companies that have put their competitors under pressure with initiatives for best-practice governance and transparent reporting. Some stock exchanges are carving out site advantages by issuing best-practice statements. This shows that differentiated initiatives establish competitive advantages and can thus have a positive impact on corporate values.

Important initiatives that promote transparent reporting come from investors

Investors are making a significant contribution to greater transparency in corporate reporting. Currently, for example, the Net-Zero Asset Owner Alliance supported by the United Nations aims to make its members’ investment portfolios climate-neutral by 2050. With this initiative, issuers of securities are asked to create scientifically based target paths for achieving the 1.5°C goal laid down by the Paris Climate Agreement from 2015. This primarily aims to internalize external costs caused by climate change. But such information can only be complete if, in addition to the greenhouse gases emitted by business activities, the activities associated with the company’s capital investments are also included. So far, this aspect has been disregarded by regulation. We believe this will change in the future.

Even if companies are required to fully disclose their investments in future, asset managers, in their fiduciary role toward investors, will still be required to screen investments for inconsistencies in terms of sustainable principles. For example, if a listed company proclaims respect for human rights in its supply chains but invests in securities that disregard them, exclusion of this issuer from the investment universe could be justified.

The bottom line

A company’s sustainability promise should be credible, comprehensible and effective. It should also be reflected in its capital investments, which will be scrutinized even more closely for contradictions in the future, not least by the regulatory authorities. As investors increasingly differentiate between companies with best-practice governance and those lagging behind, issuers of securities that pave the way have a competitive advantage.

In concrete terms, this means anticipating regulations, setting standards, eliminating reputational risks and optimizing risk-return profiles in investment strategies. An intrinsically motivated initiative for more transparency in sustainable reporting not only has advantages for refinancing the business model but also reduces implementation costs for future regulation. Expertise that is built up internally with foresight does not have to be purchased externally.

Jan Rabe is co-head of the sustainable investment office at Metzler Asset Management

Disclaimer

This information is not intended for private investors. Metzler Asset Management does not guarantee the accuracy or completeness of the information presented here. Please see our complete disclaimer at www.metzler.com/disclaimer-mam-en.

Jan Rabe

In his role as co-head of the sustainable investment office at Metzler Asset Management, Jan Rabe is responsible for the integration of ESG into portfolio management and oversees the firm's ESG investment strategy. Prior to his role at Metzler, Jan...

matters")